Livrare gratuită pentru comenzile peste 349,00 lei.

Faceți parte dintr-o comunitate de iubitori de cărți din întreaga lume și beneficiați de o mulțime de avantaje

Creați-vă un cont gratuit

Transport gratuit la punctele de livrare Pick Up peste 349.00 lei

Packeta 15.00 lei

Serviciul de curierat Cargus 28.00 lei

Easybox 20.00 lei

FAN Courier 20.00 lei

Punct FAN 16.00 lei

Punct DPD 17.00 lei

Curier Sameday 24.00 lei

Curier DPD 25.00 lei

Contact

Contact Cum să cumpăr

Cum să cumpăr

Ajutor

Livrare

Packeta 15.00 lei

Serviciul de curierat Cargus 28.00 lei

Easybox 20.00 lei

FAN Courier 20.00 lei

Punct FAN 16.00 lei

Punct DPD 17.00 lei

Curier Sameday 24.00 lei

Curier DPD 25.00 lei

Transport gratuit la punctele de livrare Pick Up peste 349.00 lei

Consilier de cumpărături

Suntem aici pentru tine!

031 22 95 182

Contul meu

▸

Gol :-(

0

Livrare gratuită pentru comenzile peste 349,00 lei.

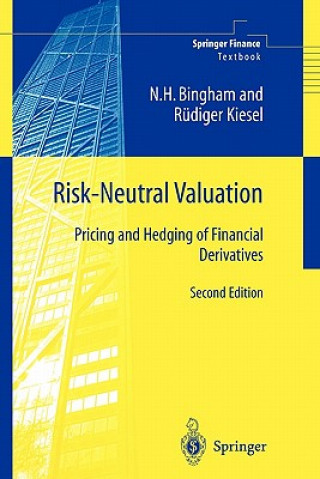

Risk-Neutral Valuation

Pricing and Hedging of Financial Derivatives

Limba

engleză

engleză

engleză

Carte

Carte broșată

This second edition - completely up to date with new exercises - provides a comprehensive and self-c...

Descrierea completă

Codul Libristo: 01434764

?

167 b

167 b

167 b

362.30

lei

În depozitul extern

Expediem în 5-8 zile

Până la 30 de zile pentru returnare

Clienții au cumpărat de asemenea

/

/

Carte broșată

Carte broșată

81.53

lei

81.53

lei

/

Carte broșată

246.58

lei

/

Carte broșată

246.58

lei

/

Carte broșată

80.08

lei

/

Carte broșată

80.08

lei

/

Carte broșată

128.06

lei

/

Carte broșată

128.06

lei

/

Foaie

71.97

lei

/

Foaie

71.97

lei

This second edition - completely up to date with new exercises - provides a comprehensive and self-contained treatment of the probabilistic theory behind the risk-neutral valuation principle and its application to the pricing and hedging of financial derivatives. On the probabilistic side, both discrete- and continuous-time stochastic processes are treated, with special emphasis on martingale theory, stochastic integration and change-of-measure techniques. Based on firm probabilistic foundations, general properties of discrete- and continuous-time financial market models are discussed.

Actriță

&

Poliglotă

EWA KASP

pentru

Redă videoclipul

Libristo are cea mai mare selecție de literatură în limbi străine. De aceea îmi cumpăr cărțile de aici.

Informații despre carte

Titlu complet

Risk-Neutral Valuation

Limba

engleză

engleză

Legare

Carte - Carte broșată

Data publicării

2010

Număr pagini

438

EAN

9781849968737

ISBN

184996873X

Codul Libristo

01434764

Editura

Springer London Ltd

Greutatea

682

Dimensiuni

158 x 233 x 24

Dăruiește această carte chiar astăzi

Este foarte ușor

1 Adaugă cartea în coș și selectează Livrează ca un cadou 2 Îți vom trimite un voucher în schimb 3 Cartea va ajunge direct la adresa destinataruluiAr putea de asemenea, să te intereseze

/

Copertă tare

690.01

lei

/

Copertă tare

690.01

lei

Consilier de cărți Libroamiko

Prin utilizarea acestui chat, comunicați cu inteligența artificială generativă. Prin utilizarea acestuia, sunteți de asemenea de acord cu prelucrarea datelor cu caracter personal.

Bună ziua! Sunt Libroamiko, consilierul dumneavoastră de cărți.

Cu ce vă pot ajuta?

Bună ziua, sunt Libroamiko, vă pot ajuta?